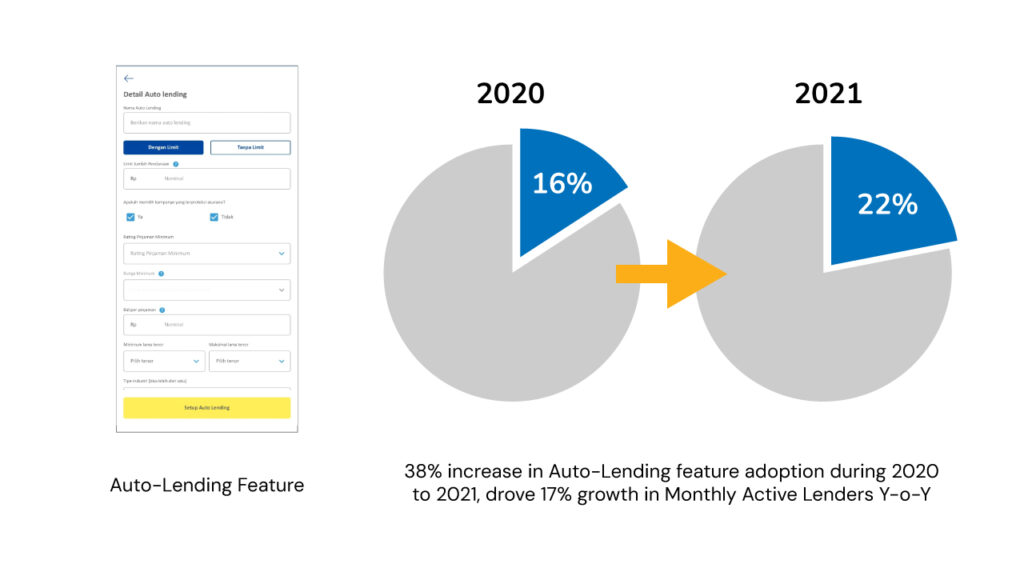

Auto-Lending Feature Adoption

Company

Akseleran

Project Type

Feature Development

Product Marketing

Duration

12 Months

Related Teams

Engineering

Marketing Team

Role

CMO – Project Owner

Lending money through a P2P lending platform like Akseleran functions similarly to an investment—lenders earn interest as returns, but they also assume risk, including the possibility of non-performing loans (NPLs).

In 2017, when Akseleran was founded, only 1% of Indonesians participated in the stock market, revealing a population more accustomed to saving than investing. This highlighted two critical gaps: low financial literacy and the need to cultivate long-term investing behaviors.

After two years of market education, we recognized an opportunity to accelerate this shift. The next step? Introducing a habit-forming feature designed to drive adoption and reinforce consistent investment practices.

Process & Solution

To make the investing activities a habit, it can followed a framework. One of the most famous frameworks for forming habit is from Nir Eyal in his book Hooked: How to Build Habit-Forming Products.

One of the phases in his framework is Action: “The action is the simplest behavior in anticipation of a reward.”

But for users to take action, the product must:

• Have high motivation

• Have high ability (i.e., low friction)

• Be paired with a trigger

This concept is heavily inspired by BJ Fogg’s Behavior Model, which Nir cites:

• B = MAT

• Behavior = Motivation × Ability × Trigger

If ability (ease of use) is low — meaning there’s too much friction — even highly motivated users may fail to act.

One of the main frictions we identified was that many users simply didn’t have the time to review individual campaign details to determine whether they met their lending and risk criteria. This led to missed opportunities for both users and the company.

Inspired by auto-debit features in traditional banking, we introduced an auto-lending feature.

In this feature, “auto” refers only to the automatic allocation of available funds in a user’s account. The lending criteria, such as minimum credit rating, interest rate, and tenor, are fully set by the user. This ensures that auto-lending only matches campaigns that align with their pre-defined preferences.

To drive adoption of the auto-lending feature, we implemented a multi-channel engagement strategy:

Onboarding Drip Campaign

Integrated auto-lending promotion into the new user email series to educate users early.

High-Touch Relationship Management

Trained Relationship Managers (RMs) to proactively highlight auto-lending benefits for high-value users.

Lender Engagement Events

Featured auto-lending in all periodic online/offline gatherings, with dedicated slides and live demos.

We complemented this with a data-driven segmented approach:

• Targeted users with high transaction frequency but irregular activity (not investing every month) to convert them into consistent lenders.

• Focused on high-value but inactive users (≤3 transactions in 90 days) to re-engage them.

For these segments, we deployed tailored retention incentives (e.g., promo vouchers).

Benefit / Result

The launch and scaling of our auto-lending feature delivered measurable business impact:

✔ 38% YoY increase in auto-lending adoption – demonstrating strong product-market fit

✔ 17% YoY growth in Monthly Active Lenders – driving platform liquidity

This adoption translated into more consistent lending behavior, with users automating their investments monthly. The rise in engaged lenders was particularly significant as it:

✔ Created sustainable platform liquidity

✔ Reduced user churn through habitual engagement

✔ Directly supported our long-term growth objectives by building reliable transaction volume